|

Accounting/Ledger

|

|

|

Accounting/Ledger

|

|

Accounting / Ledger

General The Class Accounting Ledger has been

designed to produce a controlled ledger, but with specific emphasis on debt

collection. The suggestions set out below are

those of Infospeed, and represent only one view. As with all financial issues,

you are advised to seek the advice of your accountants. Set Up Before starting to use the ledger, please ensure the

following settings are complete, especially exchange rate

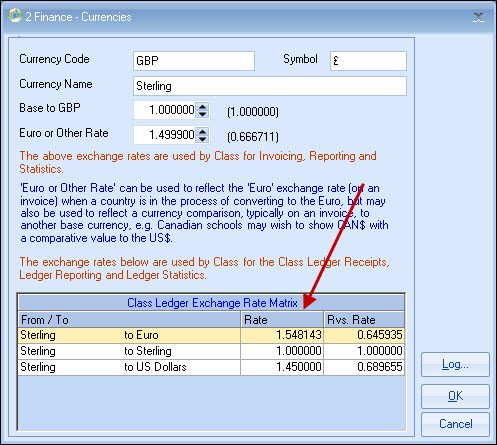

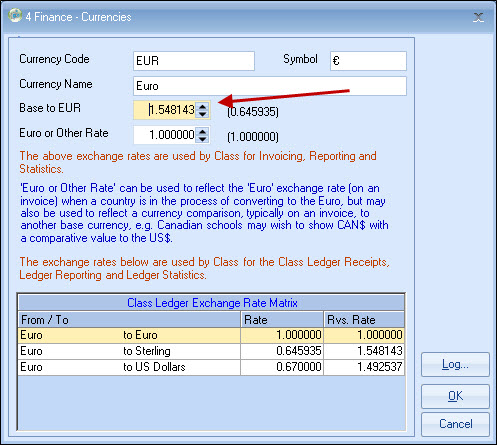

values. Set up items in the sequence below: Currencies - Exchange

Rates Typical setup for GBP to other currencies: Typical set up for other currencies - to GBP: A normal setup will show "Base to Euro" (example

immediately above) and "Sterling to Euro" (example further above) as the same

value of 1.548143. The reciprocal value of each currency is automatically

set eg. GBP to EUR = 1.548143, then EUR to GBP is automatically set = 0.645935 (as

per above example). If you alter 0.0.645935, then 1.548143 will automatically change

etc. Account Code

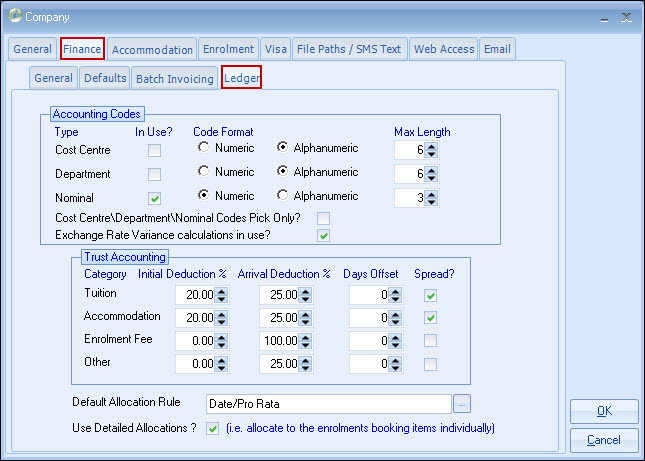

Structure The top section (Accounting Codes)

establishes whether Cost Centres, Department and Nominal Codes are in

use. Larger school setting: Default Allocation Rule Also set your Cost Centre and Department Codes if in

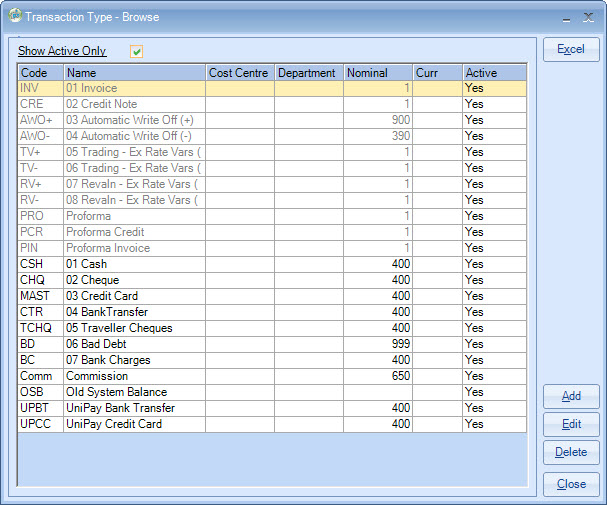

use: Nominal Codes Set up the Nominal Codes (mandatory). Transaction Types Note: numbers have been used to prefix

descriptions to show items in logical order. They are sorted in most displays,

alphabetically. The ledger has been constructed to provide

information for schools based around "Cash Accounting" or "Invoice

Accounting". Cash Accounting

As a receipt is entered, Class will allocate the value

across the enrolment elements, ie. tuition, accommodation, transfers etc.

according to a set of rules. Income can

easily be monitored, day by day, week by week, or month by month

etc. At the end of an accounting period, a report can

be produced to give an approximation of any "forward" income, ie. receipts from enrolments

which complete after the period end. Money received after

a

period end for an enrolment within the period (eg. late payment) is considered as

income in the period of receipt. Example: only tuition and accommodation

are considered. Enrolment value £12000 covering period 1/3/2012 -

1/3/2013 Invoice Accounting

This is the preferred and most accurate way of accounting

for a language school. Income is derived from invoice/credit note values, not

receipts. Invoices/credits for the period are analysed by the

system, by nominal code, for posting to the accounting system, by

journal. Invoiced sales are reduced by forward income. This is

calculated by producing an Invoice Statistical report, which analyses the

income of all booking elements spread over their duration, eg. the income

for a 12 month booking would be spread over 12 months. The recommended process is for "registrars" to produce

proformas which are sent with a booking confirmation, with finance responsible

for producing invoices. (For information, there is a permission which can block

users from producing invoices). In practice, this means an agent receives proformas all

the time (although he thinks they are invoices!) and the invoice is produced

only by finance (batch process) and acts purely as an accounting document and

generally not sent to the agent. (In value, it is the same as

the proforma). Example processes: 1. 2. This weekly invoice print (printing may also mean

emailing) run might be done on a Thursday following the weekend's arrivals. This

allows initial booking changes to be completed before converting to an invoice.

It is useful to minimise the number of invoices/credits produced and

this can be done by delaying conversion to an invoice. Some schools may decide

only to convert to invoices when required to do so for accounting purposes,

this can be after the accounting period end. If agents are set with Finance rule, "Print Invoice if

same as Proforma" = No, then generally no invoices will be sent to the

agent/student during the batch invoice run. In summary, we recommend proformas are sent to the

agent/student and converted to invoices only after arrival,

via the invoice batch print run. a) Debt collection is not dependent on an invoice (or a

proforma) being produced. Debt values occur directly from the booking itself and

receipts are entered against the booking (not the invoice/credit, as in a

traditional sales ledger system). b) If the agent will not accept proformas (unusual)

you can set the agent finance record to "Send Customer Proformas" =

No, this will force only invoices/credits to be produced. c) After the student arrives and then makes further

changes to his enrolments, we suggest the registrar continues to produce

proformas, which would be regularly converted to invoices by the batch invoice

print run. This provides a simple single rule for registrars - "Only Produce Proformas". Although

no harm occurs if invoices are accidentally produced by the

registrar. Deferred Income

As Class (from invoices) creates the sale in the

"invoice

created period", it is necessary to reduce the sales value in the

accounts by the amount of the forward sales (often called deferred

income). Reporting/Statistics

Generator/Invoicing: It is recommended that deferred income (invoices/credit

notes) from this Nominal Analysis be posted on a monthly (or whatever accounting

period is in operation) basis. The accounting entry would be reversed out for

the next accounting period. Foreign Currency

Issues Example: Accounting: Bank Statement: Debit Exchange difference - £1.67 What if the difference is to be charged to the ledger

account? What if a foreign currency ($) bank account is used to

settle a £ account instead of paying into a base currency (Sterling)

account?

Example: $1000 received and credited to the

ledger account @ 0.67 = £666.67 (It is likely that the exchange rate used will not be the

rate used for valuing the $ account in the nominal ledger, ie. the rate is

likely to be a "current" rate). Accounting: Exchange rate differences will occur when revaluing the

dollars at the accounting

period end (in total). The $ bank account = $20,000 If the exchange rate for $'s at the period end is 0.68,

then a provision would be made for the exchange rate difference as

follows:

Debit $ bank account - £600

The layout and approach is different from most accounting ledgers

to allow the specific requirements of schools to be incorporated.

Please double-click these values before proceeding.

Maintenance/Settings

> General Settings > Company > Company

You will need to set at least the Nominal Codes to be in use.

Cost Centre =

Company

Department = School/Admin

Nominal = Specific items such as

tuition, accommodation, overheads etc.

Set whether codes are to be purely

numeric or not, and the maximum length of code.

Trust

Accounting

(mainly Australia/New Zealand)

See "Company Settings -

ledger" for parameters

Set the

default allocation rule (Maintenance/Settings > General Settings >

Accounting > Allocation Rules)

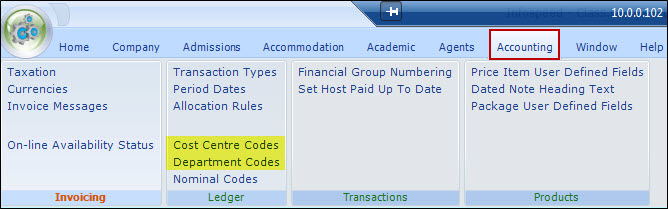

Maintenance/Settings >

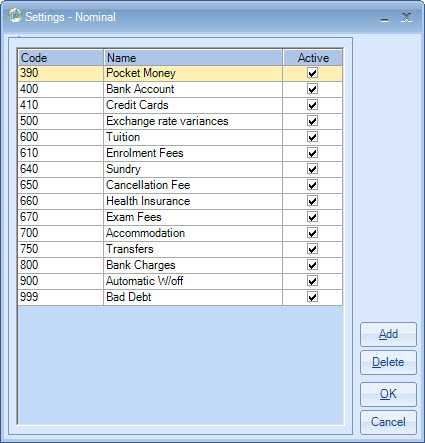

General Settings > Accounting > Nominal Codes

If Class has

been in use prior to the introduction of the ledger, you will need to create the

accounting codes already in use in your price lists.

Maintenance/Settings >

General Settings > Accounting > Transaction Types

You are now ready to start using the ledger, but you may

find the rest of this section useful to read before you start, especially the

section dealing with "opening balances".

Accounting Principles /

Issues

The first uses actual receipts as the basis for

determining income, whereas the second uses invoices/credits as the

basis.

Both are discussed in more detail below.

The rules are defined by the user, for

example money can be spread evenly across the enrolment, or it could be

allocated to accommodation first, and tuition second. The rule mechanism allows

a wide range of options, or if required the user can specify the allocation

manually at the point of entry.

Year 1/1/2012-31/12/2012

If all had been paid, then 3/12ths would be considered "forward"

income.

If £9000 has been paid, then no "forward" income would apply.

(The Nominal Ledger report is in Excel and it may be possible

for the accounting system to directly import the values from the spreadsheet,

alternatively, it can be manually posted).

Enrolments entered and proformas (not invoices)

sent to agent/student, generally by email, directly from Class. The proforma is

often called a "Booking Confirmation" and has a reference number (agent/student

number) as its identification - not an invoice number!

On a weekly basis (or less frequently if

decided by finance) an invoice batch run is completed, which converts all

proformas into invoices for arrivals up to

dd/mm/yy. The date here is normally "last weekend".

3. A few points to bear in mind:

If you would like to discuss these

principles, please contact Support.

This is done via an Excel report as follows:

These are normally sample reports already set up for

this purpose, but if not, contact Support for examples.

The report is

normally set to show income (for future periods) by Nominal Code, to allow a

prepayment journal to be prepared.

Foreign

currency paid into a base currency (eg. Sterling) account could have the

following accounting entries.

$1000

received and credited to the account @ 0.67 = £666.67.

Actual credit on bank

statement £665.00

Ledger - debit bank £666.67

Ledger - credit

debtors - £666.67

In reconciling the bank statement with

the cashbook, a £1.67 difference will show. This would be rectified by writing

off the variance as follows:

Credit Bank - £1.67

A negative *receipt can be entered and charged to the appropriate

ledger/student enrolment.

(*Alternatively, a new receipt transaction type

could be set up - "Exchange Differences". The Nominal code would credit

bank/debit debtors. This would be cleared by a receipt of £1.67).

Ledger - debit bank £666.67

Ledger -

credit debtors - £666.67

The nominal ledger

balance =

$13,000

$20,000 x 0.68 =

£13,600

Credit Exchange Rate gain/loss provision -

£600